I’ve closed Windsor Cay buyers on all four of the loan paths in this guide. Pick the wrong one and it costs you 0.75% on the rate, $25,000 in prepayment penalties, or a denied loan application three days before closing.

Here’s the part most agents won’t tell you: the loan that gets you the lowest rate at Windsor Cay isn’t always the one your lender pushes first. It depends on whether you’ll use the home personally, what your tax returns actually show, how many properties you already own, and whether Pulte Mortgage’s incentive is real money or just a number on a flyer.

I’m Mike Chen — licensed Florida Realtor® at La Rosa Realty Celebration, owner of FunStay Homes, Airbnb Superhost, and a vacation home investor with skin in this game. Let me walk you through the four ways to finance a Windsor Cay home, the math behind each one, and the rule almost nobody on the internet quotes correctly.

The 4 Loan Paths at a Glance

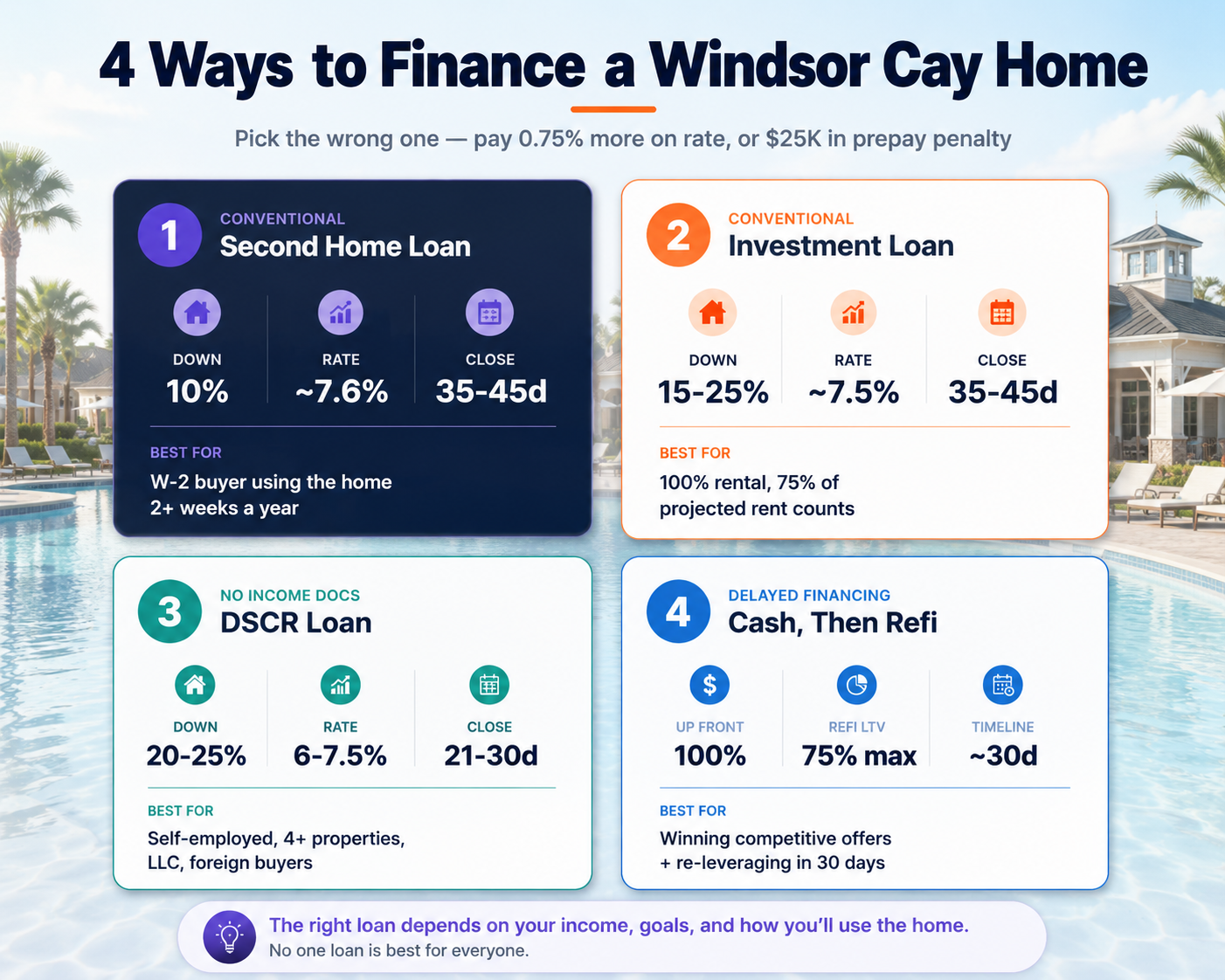

There are four real ways to buy a Windsor Cay home: a conventional second-home loan, a conventional investment-property loan, a DSCR loan, or cash followed by a delayed-financing refinance. The right one depends on your tax returns, your timeline, and whether you’ll personally use the home.

Here’s the side-by-side for a hypothetical 8-bed Windsor Cay home at $750,000.

| Second Home | Investment | DSCR | Cash + Delayed Refi | |

|---|---|---|---|---|

| Minimum down | 10% ($75K) | 15–25% ($112K–$187K) | 20–25% ($150K–$187K) | 100% up front, ~25% after refi |

| Rate (June 2026 est.) | ~7.4% | ~7.5% | ~7.0–7.5% | ~7.4% (at refi) |

| Income docs | Full (W-2 + tax returns) | Full (W-2 + tax returns) | None | None at refi |

| Rental income counted for qualifying | No | Yes (75%) | Yes (DSCR-based) | Yes (DSCR-based) |

| Closes in LLC? | No | Sometimes | Yes | Yes |

| Prepayment penalty | No | No | Usually (5/4/3/2/1) | No |

| Time to close | 35–45 days | 35–45 days | 21–30 days | Same week + 30-day refi |

| Best for | W-2 buyer using home personally | W-2 buyer maxing borrow power | Investor scaling / 4+ properties / foreign buyer | Competitive offer + re-leverage |

Now let me explain each one in plain English, with real Windsor Cay numbers.

Can I Use a Second-Home Loan for a Windsor Cay Airbnb?

Yes, and this is the path most of my W-2 buyers want. Under Fannie Mae Selling Guide section B2-1.1-01, you can short-term rent your Windsor Cay home on Airbnb and VRBO and still qualify for a second-home loan, as long as you keep exclusive control and don’t sign into a rental pool.

That’s the rule almost nobody on the internet gets right.

Here’s what Fannie Mae actually requires for a second-home loan:

✔️ Must be occupied by the borrower for some portion of the year

✔️ Must be a one-unit dwelling, suitable for year-round occupancy

✔️ Borrower must have exclusive control over the property

✔️ Must not be subject to any agreement that gives a management firm control over the occupancy of the property

What this means at Windsor Cay: A normal property-management setup where you can block any date on your own calendar (the way FunStay and any legitimate STR manager structures it) clears the bar. An exclusive rental-pool agreement where the manager controls when guests check in without your veto disqualifies the property. Know the difference before you sign anything.

The numbers

- Minimum down: 10%

- Credit floor: 640 with 25% down + DTI under 36%; otherwise 680+

- Rate: ~7.60% on a 720 FICO loan as of April 2026 (Curinos data)

- Reserves: 2–6 months of PITI

When I recommend it

You make solid W-2 income, you’ll actually use the home a couple of weeks a year, and you don’t need Airbnb income to qualify. Cheapest path, lowest down payment, no prepay penalty.

When You Want an Investment-Property Loan Instead

Pick the investment-property route when you’ll never personally use the home and you want 75% of projected rental income to count toward qualifying. An investment loan lets the property’s expected rent help you qualify, a second-home loan does not.

The numbers

- Minimum down: 15% (with top-tier credit), 20–25% is standard

- Credit floor: 680–700; you need 700+ if you’re putting less than 25% down

- DTI cap: 45%

- Rate: ~7.18% to 7.68% as of late May 2026

- Reserves: 6 months of PITI

The Loan-Level Price Adjustment (LLPA) stack on investment properties is heavier than second homes, which is why the rate runs roughly a full point above primary residence. If your plan is 100% rental and you don’t want any underwriting questions about how often you’ll visit, this is the cleaner path.

What Is a DSCR Loan and Why Most Windsor Cay Investors Use One

A DSCR loan qualifies you on the property’s rental income, not your personal tax returns. That’s why it’s become the default loan for serious vacation-rental investors at Windsor Cay, Reunion, ChampionsGate, and the rest of the Disney-area corridor.

DSCR stands for Debt Service Coverage Ratio. The math is simple:

DSCR = Gross Monthly Rent ÷ PITIA (PITIA = Principal + Interest + Taxes + Insurance + HOA)

If the ratio is 1.00 or higher, the property covers its own debt. Most lenders want 1.25 or better to unlock the best pricing and maximum leverage.

The numbers

- Down payment: 20% (with 700+ FICO and DSCR of 1.25+); 25% is standard

- Credit floor: 620 absolute minimum; 660–680 typical; 700+ for top tier

- Rate (May 2026): 6.125% to 7.5% on the cleanest deals; up to 10.75% on stretched ones

- Reserves: 6 months of PITIA (some lenders accept 3 months)

- Closes in: LLC name, no problem

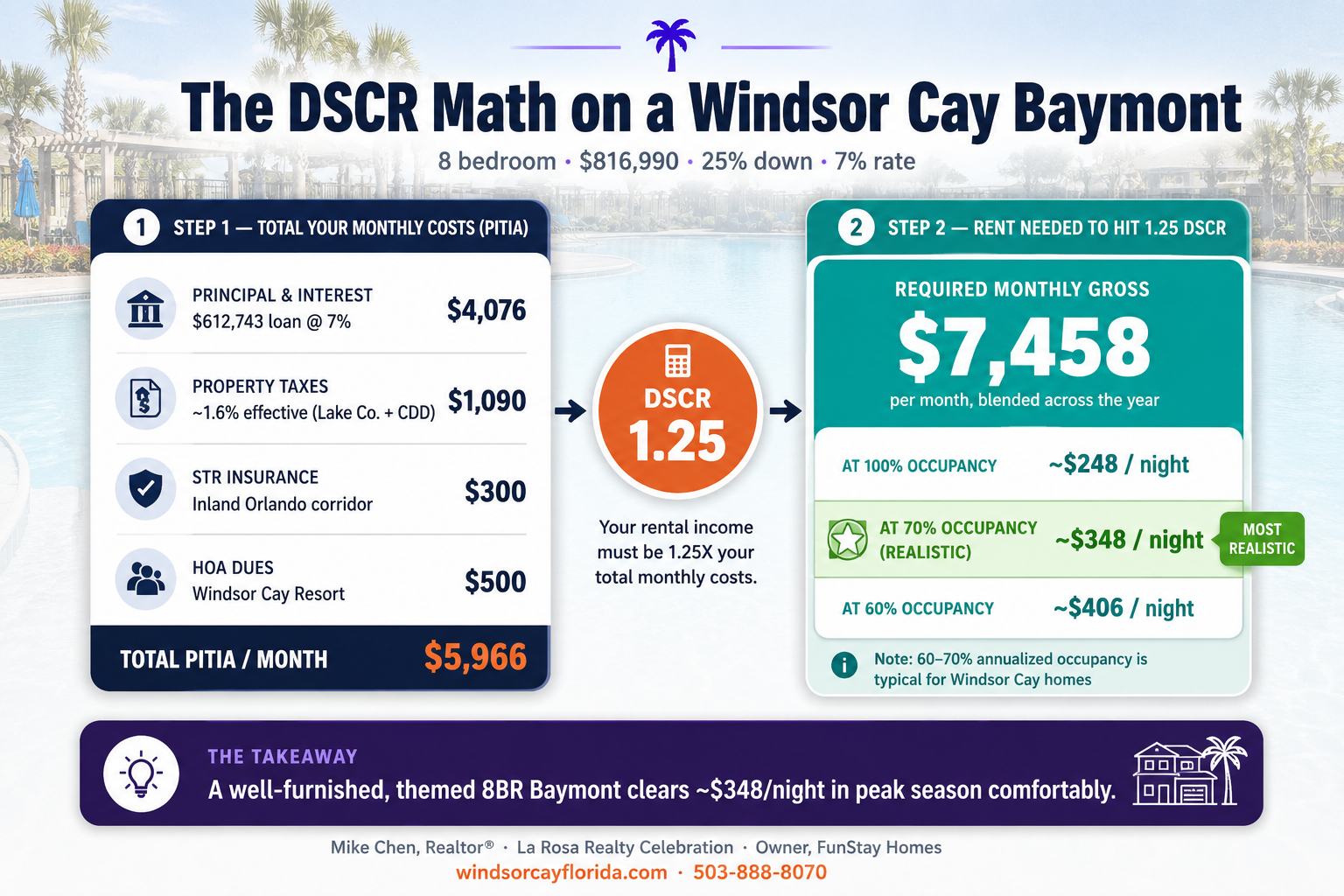

Real Windsor Cay DSCR math

Let’s run the 8-bed Baymont model at $816,990 (current Pulte pricing).

- 25% down → loan amount of $612,743

- At a 7% rate, principal + interest ≈ $4,076/month

- Property taxes at 1.6% effective → $1,090/month

- STR insurance → $300/month

- HOA → $500/month

- Total PITIA ≈ $5,966/month

To hit a 1.25 DSCR, the home needs to gross $7,458/month in rent. That’s about $248/night at 100% occupancy, or $348/night at 70% occupancy. A well-furnished, themed 8-bed Baymont clears that during peak season comfortably. The real question is the annualized blended rate. (For what actually moves the needle on bookings, see my deeper dive on what affects Airbnb income in Windsor Cay.)

The prepayment penalty trap

This is the part most DSCR articles bury. The standard DSCR prepayment penalty is a 5/4/3/2/1 step-down:

- Year 1: 5% of remaining principal

- Year 2: 4%

- Year 3: 3%

- Year 4: 2%

- Year 5: 1%

- After year 5: 0%

On a $600,000 DSCR loan paid off in year one, that’s a $30,000 hit. If you might sell or refinance within five years, ask your lender about a shorter prepay (1-year or 3-year) or a no-prepay option, both are available, both come with a slightly higher rate. Pay for the flexibility if you need it.

When I recommend DSCR

Your tax returns understate your real income (because of depreciation, write-offs, or self-employment). You already own four or more financed properties and conventional lenders are tapping out. You’re a foreign buyer with no U.S. tax history. You want to close in an LLC. Or you want to scale fast without DTI ceilings.

Should I Pay Cash for a Windsor Cay Home (Then Refinance)?

Yes, if you want to win the offer and pull most of your cash back within 30 days using Fannie Mae’s delayed financing exception.

Most buyers don’t know this exception exists. Fannie Mae’s Selling Guide B2-1.3-03 waives the standard 6-month seasoning for a cash-out refinance if you bought with cash in an arm’s-length transaction, can document the source of funds, and have clean title. You can refinance the day after closing if your lender is fast.

The catch — LTV caps

The new loan is treated as a cash-out refi, so the same caps apply:

- One-unit second home: 75% LTV max

- One-unit investment property: 75% LTV max

- 2–4 unit investment: 70% LTV max

The math

On a $600,000 all-cash purchase where the home appraises at $620,000 on an investment delayed-financing refi at 75% LTV:

- Maximum loan = the lesser of: (a) original purchase + closing costs ≈ $615K, or (b) 75% of $620K appraised value = $465K

- You pull back $465,000 and stay in roughly $135,000 — about 22% effective down

When it’s worth it

You want the strongest possible offer (cash beats financed every time, and Pulte will sharpen the pencil for cash). You expect rates to drop in the next 90 days and want to time your lock. You have the liquidity to float $500K–$1M for 30–60 days without missing it.

When it isn’t

Two sets of closing costs — figure roughly 3–4% of the loan amount in total fees, plus the Florida doc stamps and intangible tax I cover below. If you don’t need the cash flexibility, just finance the purchase normally.

Is Pulte Mortgage Actually the Cheapest Way to Finance Windsor Cay?

Sometimes, but only when the credit value beats what a competing lender’s rate saves you over the life of the loan. Don’t take the incentive at face value. Do the math.

The published Windsor Cay incentive on my pricing page is $7,500 in closing costs + $6,000 in prepaid HOA dues = $13,500 total when you finance with a preferred lender (Pulte Mortgage) or pay cash.

What’s not on the flyer: PulteGroup ran incentives at 8.7% of gross sales price in Q2 2025, up from 6.3% the year before. They’ve leaned heavily into rate buydowns. Two products to ask about:

- 2/1 buydown: Your rate is reduced by 2% in year one and 1% in year two, then returns to the note rate from year three onward

- 3/2/1 buydown: Same idea, three years of step-down (3% off in year one, 2% in year two, 1% in year three)

- Forward commitments: Pulte Mortgage buys mortgage pools at below-market rates in bulk and passes some of that savings to buyers

The honest test

Get a rate quote from one outside lender (a portfolio lender, a local credit union, or a DSCR specialist for investment plays). Compare apples to apples: same loan amount, same down payment, same term, same lock period. Then add Pulte’s $13,500 credit to the outside lender’s closing costs and see which side wins on total cost over your expected hold period, not over 30 years.

I’ve seen it go both ways. Pulte usually wins on shorter holds; an outside lender with a sharper rate often wins on 7+ year holds.

What Are Closing Costs on a Windsor Cay Home in Florida?

Plan for roughly 1–2% of the purchase price in Florida-mandated state taxes alone, before any lender or title fees. Florida is one of the more expensive states for recording taxes, and Lake County doesn’t add a local surcharge (only Miami-Dade does).

On a $700,000 purchase with a $560,000 mortgage:

| Tax | Rate | Cost |

|---|---|---|

| Doc stamps on the deed (seller-paid by convention) | $0.70 per $100 of price | $4,900 |

| Doc stamps on the note/mortgage (buyer-paid) | $0.35 per $100 of loan | $1,960 |

| Intangible tax on the mortgage (buyer-paid) | 2 mills per $1 of loan | $1,120 |

| Total state recording taxes | ~$7,980 |

These rates come straight from the Florida Department of Revenue. The buyer’s side on a $560K loan is about $3,080 in mandatory state taxes before any title insurance, lender, or escrow fees.

Then there’s annual property tax. Per the Lake County Property Appraiser, Lake County millage runs around 5.0254 (general fund) plus 6.0850 (school), and including CDD assessments at Windsor Cay, you’re looking at an effective annual rate of about 1.6% of assessed value — which is exactly what I publish on the Fees page. For a deeper breakdown, see my complete HOA, CDD, and property taxes guide.

One more thing buyers miss: Florida’s homestead protection caps annual assessment increases at 3%, but Windsor Cay STRs don’t qualify for homestead, so you’re under the 10% non-homestead cap instead. Your tax bill can grow faster than a primary-residence owner’s.

STR Insurance: Don’t Quote a Homeowners Number

Standard HO-3 homeowners policies generally exclude business activity — meaning if a guest gets hurt or your home gets damaged during an Airbnb stay, the carrier can deny the claim. You need a real short-term-rental policy.

Budget $2,000–$4,000 per year for a full STR program (dwelling + general liability + loss of rents + contents) on an inland single-family STR in the Orlando vacation corridor. Carriers to shop: Proper Insurance, Steadily, Slice, Allstate Host Advantage, Farmers’ STR product. And don’t forget the wind/named-storm deductible. It’s a separate 2%–10% of dwelling value on most Florida policies, even inland.

What Loan Should You Actually Pick? (My Honest Recommendation)

This is the framework I walk every Windsor Cay buyer through:

✔️ W-2 income, planning to use the home 2+ weeks a year → Second-home loan. Cheapest down, lowest rate, no prepay.

✔️ High W-2 income, never personally using the home → Investment loan. Rental income counts toward qualifying.

✔️ Tax returns understate your income, or you’re scaling past 4 properties → DSCR. No income docs, LLC-friendly.

✔️ Foreign buyer with no U.S. credit history → DSCR. Specialized lenders accept ITINs and foreign-bank statements.

✔️ Need to win a competitive offer and you have the liquidity → Cash + delayed-financing refi. Win on the offer, re-leverage in 30 days.

One more thing and this is on me as the agent, not your loan officer: always confirm qualification with a lender before you write an offer. Rate quotes are perishable and rules change. My job is to point you at the right path; your lender’s job is to put you in the right loan.

For more on the buyer-side mistakes that quietly tank deals, see Top Mistakes Buyers Make in Windsor Cay.

Frequently Asked Questions

Can I get a second-home loan for a Windsor Cay Airbnb?

Yes. Under Fannie Mae Selling Guide B2-1.1-01, you can short-term rent a second home on Airbnb and VRBO as long as you occupy it for some portion of the year, keep exclusive control, and don’t sign into a rental-pool agreement. Rental income cannot be used to qualify on a second-home loan.

What credit score do I need for a DSCR loan in Florida?

Most DSCR lenders require a minimum FICO score of 620. To unlock the best rates, larger loan amounts, and 20% down payment options, you typically need a 700+ FICO. Anything below 660 will push you into the higher end of the rate range (8%+).

How much down payment do I need for a Windsor Cay home?

Down payment minimums vary by loan type: 10% for a conventional second-home loan, 15–25% for a conventional investment loan, 20–25% for a DSCR loan, or 100% up front if you’re doing cash with a delayed-financing refi planned within 30 days.

Does my Airbnb income count toward qualifying for a mortgage?

On a conventional second-home loan, no. On a conventional investment-property loan, yes Fannie Mae allows 75% of documented or projected rental income. On a DSCR loan, the property’s rent is the only qualifying factor; your personal income is irrelevant.

Can a foreign buyer get a DSCR loan in Florida?

Yes. Many DSCR lenders accept foreign-national borrowers with a passport, ITIN, and U.S. bank account, no Social Security number or U.S. credit history required. Down payment is typically 25–30% and rates run slightly higher than domestic DSCR pricing.

What is the prepayment penalty on a DSCR loan?

The industry standard is a 5/4/3/2/1 step-down: 5% of the remaining principal in year one, declining by one percentage point each year, with no penalty after year five. On a $500,000 loan paid off in year one, that’s a $25,000 hit. Shorter prepay structures are available for a slightly higher rate.

Are Pulte Mortgage’s rates competitive?

Sometimes. Pulte Mortgage uses forward commitments and rate buydowns (2/1 and 3/2/1) to offer below-market rates on Windsor Cay homes, combined with Pulte’s $13,500 incentive package. Always get a competing quote from an outside lender and compare total cost over your expected hold period, not just the headline rate.

Can I close on a Windsor Cay home in an LLC?

On a conventional loan, no — Fannie Mae requires individual ownership at closing. On a DSCR loan, yes, and most DSCR lenders prefer it. Cash buyers can close in an LLC and then refinance into the LLC’s name as well.

Ready to Talk Through Your Numbers?

If you’re seriously evaluating a Windsor Cay home and you’re not sure which loan path fits your situation, let’s run the math together before you fill out a mortgage application. I’ll connect you with the lenders I’ve seen actually close Windsor Cay deals on each of these four paths, not the ones who only talk a good game.

Mike Chen, Realtor® — La Rosa Realty Celebration Windsor Cay specialist. Airbnb Superhost. Owner of FunStay Homes.

{kind=link}